Summary

This is a TEMP CHECK to gauge community sentiment for depositing USDC reserves to sUSDS from Sky Ecosystem (ex MakerDAO). The initiative aims to increase Fluid’s revenue which will be redistributed back to the lenders therefore increasing lending APR and enhancing the protocol’s competitiveness and market positioning.

Proposal

The Instadapp & Phoenix Labs teams propose the following:

- Transfer unutilized USDC from the Liquidity Layer to sUSDS (Savings USDS)

- Redistribute generated yield back to the lenders

About sUSDS

Savings USDS is the upgraded version of sDAI, which offers a greater yield (currently 6.25 % APY - 0.25 % more than sDAI). Savings USDS are tokenized USDS deposits in the Sky Savings Rate. It’s important to note that there is no difference in risk between sUSDS and USDS, as Sky Savings Rate deposits are not lent out, or used for insurance or staking. It is simply a way to activate savings.

Sky aims to always offer the best risk-adjusted yield on stablecoins in DeFi. Sky does this through its Sky Stars and Allocation System that can deploy USDS into the best risk adjusted yield opportunities depending on the market. For example, when TradFi rates are high, Sky can deploy assets into U.S. T-Bills. On the other hand, when DeFi rates are high Sky can deploy USDS liquidity into DeFi lending markets. This ensures that USD brings a competitive yield in any market environment.

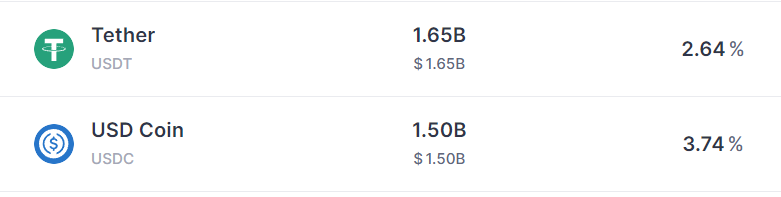

Furthermore, sUSDS is very liquid against USDC, as 25 % of USDS reserves are in liquid stablecoins, meaning sUSDS can be instantly converted to USDC in the size of billions with no slippage. Similarly, there is no limit to converting USDC to sUSDS. This makes sUSDS an incredibly flexible and low-risk yield asset.

Motivation

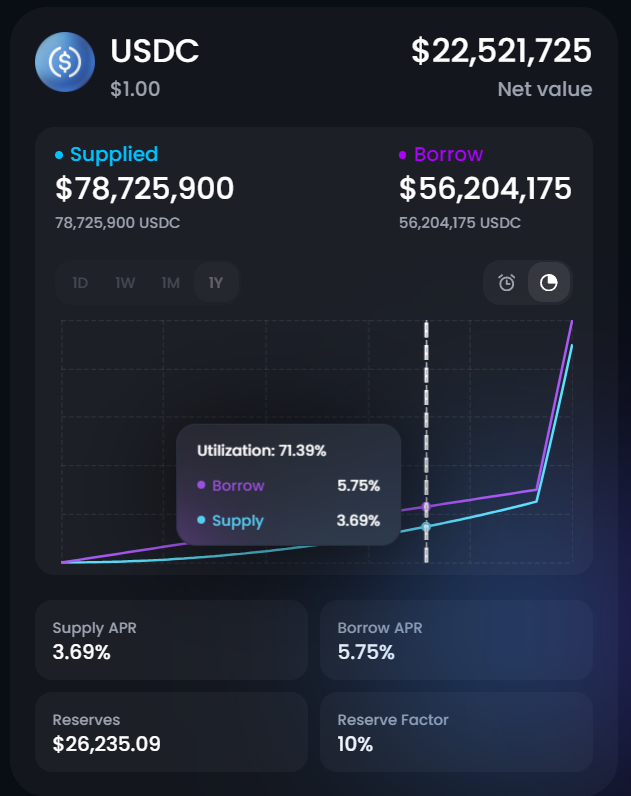

The primary motivation behind this proposal is to ensure efficient capital utilization. Currently, Fluid USDC lending market is at ~70% utilization, leaving 30% of USDC reserves sitting idle and generating no return for the lenders. Native supply APR is only 3.7% which is subsidized by the protocol’s revenue to increase it to 5.75% APY. There is very low demand for leverage on the market and all major lending markets are facing the same problem for example, Aave supply rates are 2.6% - 3.7%.

By deploying unutilized USDC into sUSDS, we aim to:

- Increase Protocol Revenue: Idle USDC can generate an additional 6% APY, enhancing overall protocol revenue. The projected 6% yield on $20M idle USDC represents $1.2M additional revenue to the lenders.

- Improve Efficiency: Idle capital represents an opportunity cost for the lenders. By converting unused reserves into productive assets, we ensure that Fluid remains competitive.

- Maintain Flexibility: sUSDS can be liquidated into USDC in the same transaction, ensuring that the protocol remains liquid and can meet borrower demand in the event of an increase in USDC utilization or USDC withdrawals.

This proposal aligns with our broader strategy to maximize capital efficiency while managing risk responsibly.

Risks

While the opportunity for additional yield is clear, there are several risks that need to be carefully considered:

-

Smart Contract Risk: Like all DeFi protocols, depositing USDC into sUSDS involves smart contract risk. However, this risk is considered low as Sky Ecosystem (MakerDAO) has been live for many years with a brilliant security track record.

-

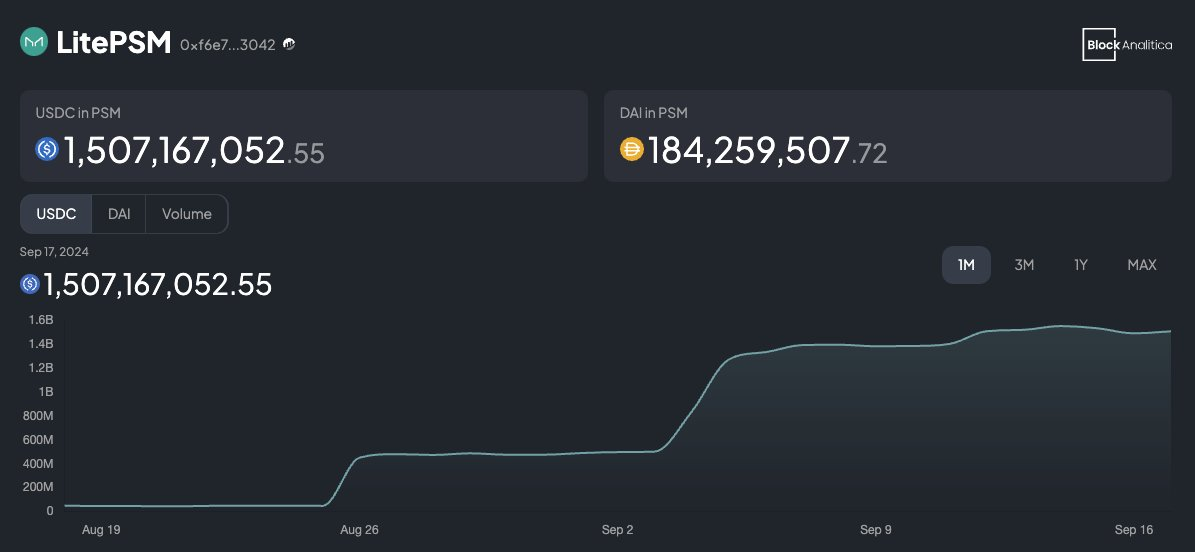

Liquidity Risk: In the event of the USDC demand, we will need to liquidate sUSDS to meet borrowing/withdrawal requirements. While sUSDS PSM has $1.5B in reserves, it can dry up in case of force major conditions making it impossible for Fluid users to withdraw USDC.

To mitigate this risk we propose to automatically withdraw USDC from sUSDS when PSM level goes below $0.5B and Fluid deposits should never exceed more than 10% of the PSM.

- USDS Depegging Risk: Although USDS (DAI) has historically maintained its peg to the U.S. dollar, this risk always exists especially considering exposure to the RWA and regulatory risks it implies.

Next Steps

Gather community feedback to initiate an on-chain proposal to

- Proceed with the suggested parameters

- Proceed with the alternative parameters

- Or not to proceed with the proposal