Introduction

Fluid Protocol has crossed $3 billion in market size, securing its position as the 4th largest money market by active loans and the 2nd largest DEX on Ethereum in volumes and fees. With an annualized revenue run rate surpassing $10 million based on recent performance, Fluid has already established itself among the top tier of DeFi protocols.

Over the past ~15 months, Fluid has achieved substantial results:

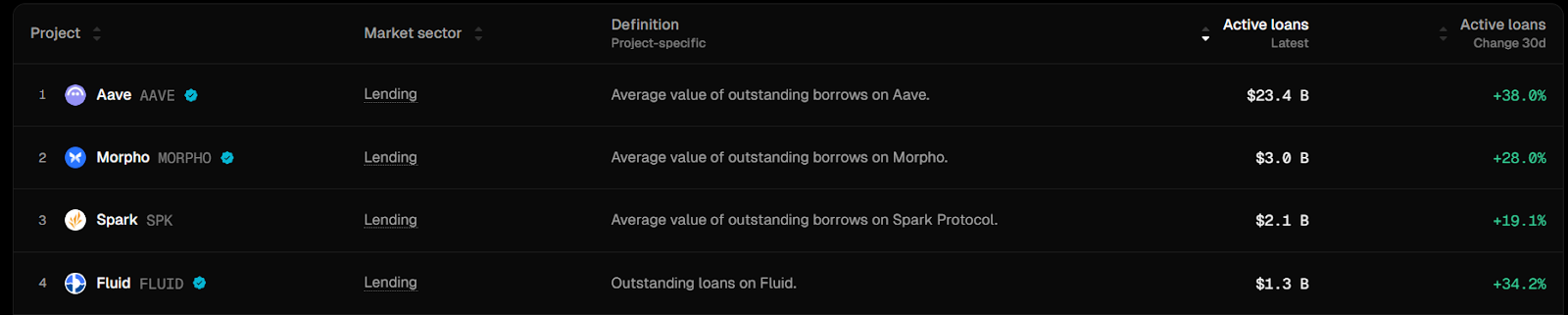

- Fluid Lending ranks among the top 4 lending markets on Ethereum by active loans:

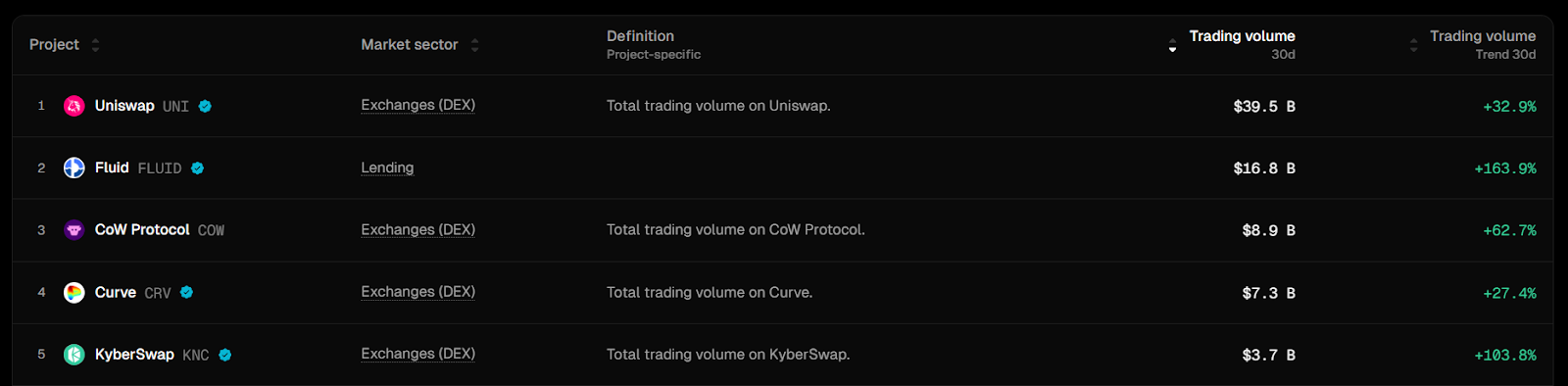

- Fluid DEX is currently the second largest by trading volume and fees on Ethereum:

These achievements mark more than just success to date - they are the base from which we accelerate toward our next milestones: $10 billion in market size and $30 million in annualized revenue over the coming six months. With multiple growth catalysts ahead, we see a clear path to scaling further, faster, and across more markets than ever before.

Why $10B and $30M Matter

Reaching these targets will position Fluid as not only a leader in individual markets, but as a cross-chain DeFi platform that commands global attention. At $10B in market size and $30M in revenue, Fluid will have:

-

The liquidity depth to power large-scale financial activity.

-

A proven, diversified revenue base that supports sustainable growth.

-

Greater ability to reinvest in technology, partnerships, and incentives.

-

A stronger position to attract more institutional adoption and long-term capital inflows.

Foundation of Fluid’s Next Growth Phase

1. Distribution Expansion

Fluid is actively building a multi-pronged distribution strategy designed to put our technology into the hands of more users and protocols worldwide.

-

Partnership-Driven Growth: Juplend serves as our pilot distribution program, combining Fluid’s advanced tech and operational expertise with Jupiter’s reach.

-

Expanding Partner Network: We are in active discussions with other distribution partners who can onboard millions of users through native integrations.

-

Multi-Chain Deployment: While growing core markets such as Ethereum, Arbitrum, and Base, we are preparing for native Fluid deployments on additional chains with high growth potential, expanding our presence and liquidity footprint.

2. Product Innovation and Growth Catalysts

Our product roadmap extends far beyond what has already been announced.

-

Upcoming Launches: DEX Lite, Jupiter Lend, USD Lite vault, and DEX V2 will significantly enhance user experience, liquidity, and revenue.

-

Future Products: Additional protocols built on top of Fluid will be announced later this year, each designed to attract new TVL and generate more DAO revenue. Things already in the ideation phase:

- Permissionless protocol (allowing risk curators to deploy vaults & DEXes using the most advanced liquidation engine).

- Fixed rates protocol.

- Perps protocol.

- Sophisticated DEX LP vault strategies.

-

Technology Leadership: Fluid’s architecture enables us to fully support user journeys end-to-end, making us the go-to DeFi infrastructure provider.

3. The $FLUID Token

The $FLUID token is central to our governance, community alignment, and long-term value creation strategy. As the protocol grows, so too will the role of the token in decision-making and value accrual. It is very important to know that Fluid protocol is fully governed by the token holders and has no material equity behind it. Fluid has scored near-perfect score in the recent Blockworks Token Transperancy report.

As the protocol continues to mature and 100% of $FLUID tokens have been vested, we are now opening a community discussion on introducing a token buyback program. Rather than imposing a single model, we are presenting multiple approaches for governance to consider.

Buyback Models for Discussion

Model 1: Dynamic Buyback Based on FDV (x * y = k)

In this model, the percentage of revenue allocated to buybacks depends on the fully diluted value (FDV) of the FLUID token. If the FDV is below $0.5 billion, 100% of revenue goes to buybacks. As the FDV increases, the percentage allocated to buybacks decreases according to the x * y = k curve.

-

Pros: This approach ensures more aggressive buybacks when the token is undervalued, potentially supporting the price during weaker market conditions.

-

Cons: It could create a perceived price ceiling, where the community might think the team doesn’t expect the token to go above certain valuations, possibly influencing market perception.

Model 2: 30-Day TWAP Buyback

This model uses the 30-day Time-Weighted Average Price (TWAP) of the token. If the current price is below the 30-day TWAP, 100% of the revenue is used for buybacks. If the current price is above the 30-day TWAP, no buybacks occur.

-

Pros: This method builds treasury reserves during bullish periods and deploys buybacks primarily in bearish conditions, aiming to support the token price when it’s under pressure.

-

Cons: It may lead to buybacks at relatively high valuations if the token has recently dipped from a peak, and it might miss opportunities to buy during gradual uptrends.

Model 3: Hybrid Approach

The hybrid model combines elements of both approaches. In bull markets, the protocol minimizes buybacks, preserving revenue. In bear markets, it applies the x * y = k model to scale buybacks based on FDV, ensuring that when the token is severely undervalued, more aggressive buybacks occur.

- Pros: Combines the strengths of both models, adapting to different market conditions and providing a balanced approach.

The team inclines towards a hybrid approach as it maintains a healthy balance between growing the treasury and purchasing the token when it is the most undervalued.

We also encourage discussion of the no-buyback option, preserving maximum revenue for reinvestment into growth

-

Preserving Liquid Reserves and Reinvesting in Growth:

In traditional business models, companies often reinvest profits to fuel further growth before considering any form of buybacks. In the Web3 space, while tokens can be used as incentives, maintaining a strong cash reserve allows for more aggressive investment into new protocols, partnerships, and user acquisition. By not spending revenue on buybacks, Fluid can potentially scale faster, attract more users, and achieve the next stage of growth more rapidly. -

Resilience During Bear Markets:

Bear markets can be challenging for any protocol. If most of the revenue has been used for buybacks, the protocol may find itself with limited cash reserves when it needs them most. Having a robust treasury means the protocol can continue innovating and even expanding during downturns, turning challenges into opportunities. It also reduces the risk of having to cut back on incentives or development due to a lack of funds. -

Long-Term Vision Over Short-Term Price Support:

While buybacks can be a way to signal alignment with token holders, it’s important to recognize that small-scale buybacks may not drastically increase the token price on their own. The real driver of long-term token value is the protocol’s future potential and growth trajectory. By focusing on reinvestment, the protocol can work toward becoming a major DeFi player with a robust suite of services, ultimately attracting investors who are looking at the protocol’s multi-year growth prospects rather than short-term price moves.

Should the community vote for a specific option following the initial discussion period, buybacks will start being implemented come October 1st. The buyback initiative, if approved by the community, will be assessed after a 6-month period to evaluate its effectiveness and impact on Fluid protocol growth.

4. Revenue Flywheel

Our growth model is designed to create a self-reinforcing loop:

Revenue Growth → Product Development & Incentives → Increased TVL → More Revenue.

-

DAO Treasury Strength: A healthy treasury ensures the DAO can finance security partners, growth initiatives, and community programs without external funding pressure.

-

Strategic Incentives: Targeted incentive programs can rapidly increase TVL and deepen liquidity in strategic markets.

-

Sustainable Scaling: Revenue growth fuels expansion across new products, partnerships, and ecosystems, accelerating progress toward $10B and beyond.

The Fluid team itself maintains a healthy balance of cash and doesn’t need to draw from the DAO treasury for at least until the end of the year to pay salaries and operational costs. However, as Fluid’s governance matures and the protocol scales across multiple chains with robust, sustainable revenue, the coming phase presents a strategic opportunity to onboard specialized third-party service providers. This includes security partners to enhance both code integrity and economic safeguards, as well as growth-focused providers to position Fluid for stronger institutional adoption. These service providers will have to be financed by the DAO.

Conclusion

This proposal is intended to foster a transparent, data-driven discussion on the most effective approach to FLUID token buybacks at this pivotal stage of the protocol’s growth. By presenting multiple models, including the possibility of no buyback, we aim to give the community the opportunity to weigh the trade-offs, align on strategic priorities, and choose a path that best supports both short-term performance and long-term value creation.

With ambitious targets ahead of $10 billion in market size and $30 million in annualized revenue within the next six months, our collective decision will shape not just immediate market dynamics, but also Fluid’s positioning as a leading DeFi protocol in the years to come. We encourage all community members to participate actively, share their perspectives, and help refine a strategy that maximizes the benefits for all stakeholders.